CoinLedger was able to go through my hundreds of Crypto and NFT transactions and help me pinpoint what needed adjusting for tax filing. Before CoinLedger, I was scared to even look at my capital gains, post CoinLedger, I'm excited. Highly recommend!

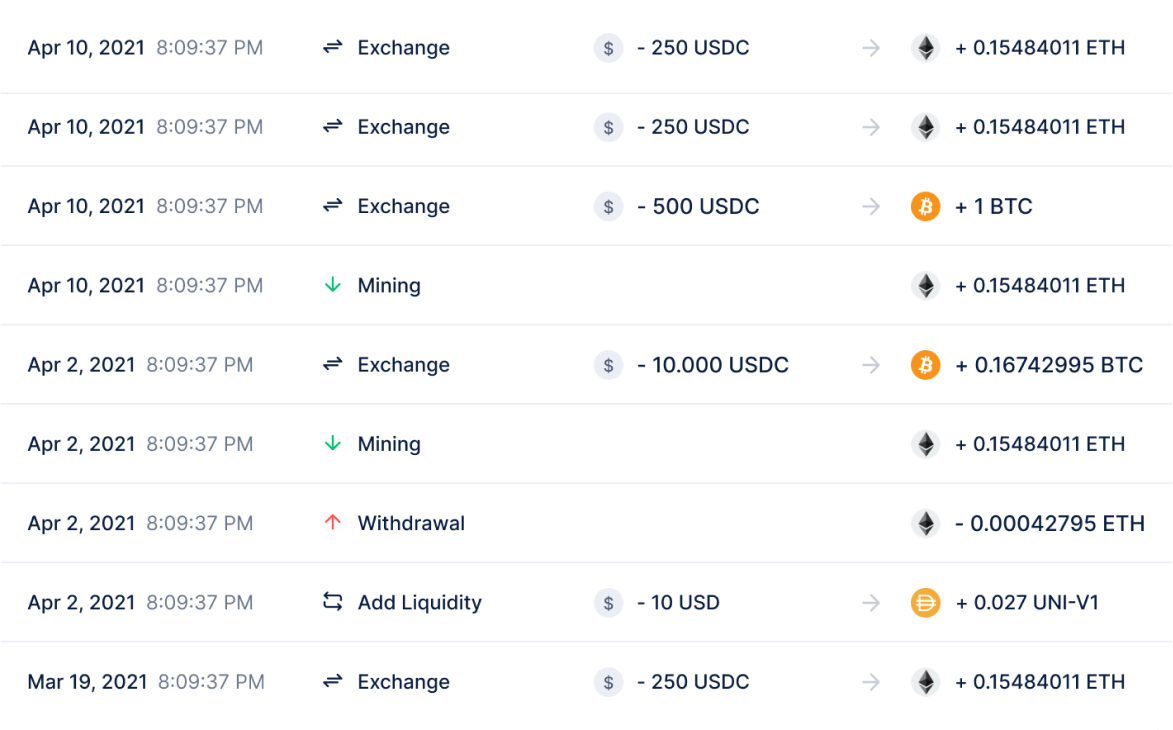

Import your crypto transactions from your wallets and exchanges.

Watch the platform calculate your gains and losses for all your transactions — trading, staking, NFTs, or anything else!

Once you view your transaction history, download your tax report with the click of a button.

Writing off crypto losses can help you save thousands. Claim your tax-savings today with CoinLedger!

Learn More

.svg)

.svg)

CoinLedger integrates directly with your favorite platforms to make it easy to import your historical transactions. Whether you’re trading, earning interest, or buying NFTs you’ll be able import your transactions and calculate your taxes with ease.

See How It WorksDownload your completed tax forms to file yourself, send to your accountant, or import into your preferred filing software.

Partnered with the largest tax preparation platform to make it easier than ever to report your crypto gains and losses. Your reports can be directly imported into TurboTax Online, TurboTax Desktop, TaxAct, and many other tax platforms!

See How it Works

Generate your crypto gains, losses, and income reports in any currency. These reports can be used to complete the relevant tax forms for your country.

Get Started For Free

This guide breaks down everything you need to know about cryptocurrency taxes, from the high level tax implications to the actual crypto tax forms you need to fill out.

The gains, losses, and income generated from your crypto investment activity needs to be reported on your taxes in your home fiat currency (e.g. USD). CryptoTrader.Tax handles this reporting automatically.

The basics of cryptocurrency taxation and how much you’ll be paying in tax.

The basics of cryptocurrency taxation and how much you’ll be paying in tax.

.png)

.png)

.png)

.png)

.webp)

.webp)

%20-%20George%20Dimov.png)

.jpeg)

.png)

.png)

.jpeg)